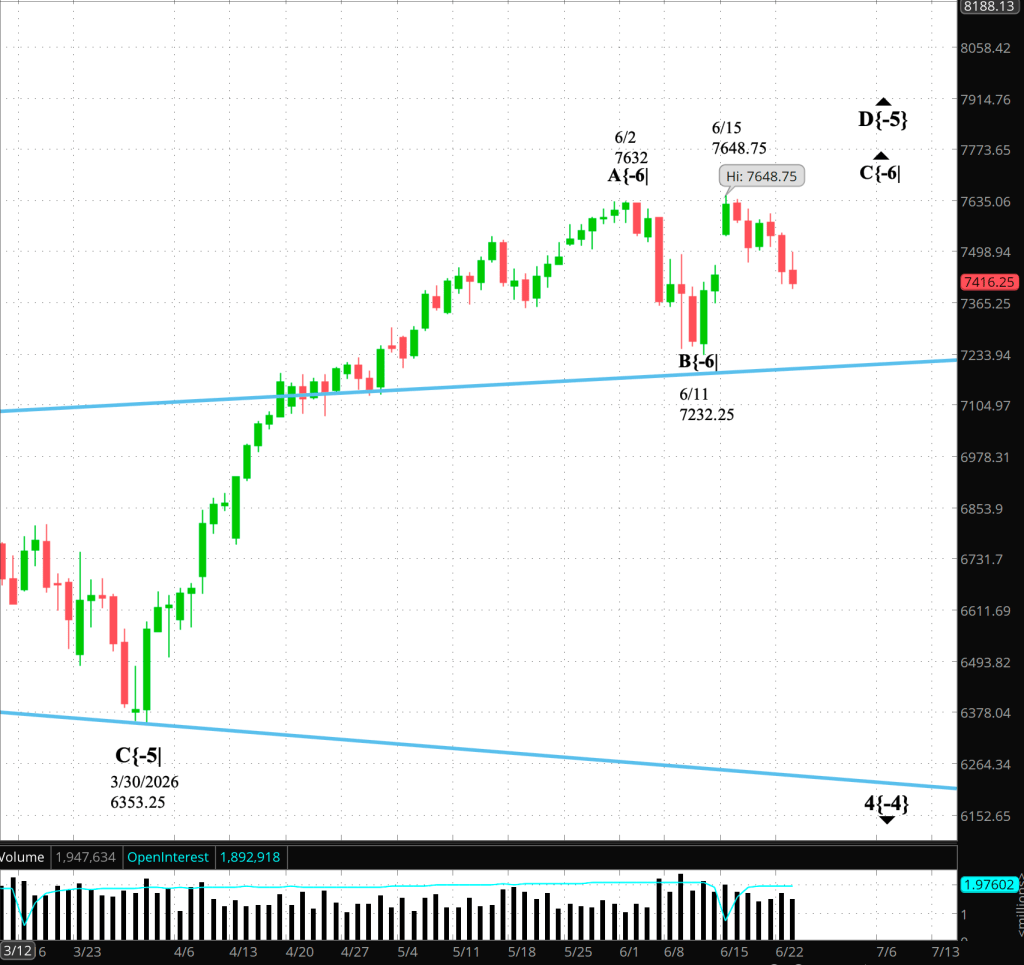

3:30 p.m. New York time

Half an hour before the closing bell. The S&P 500 futures fell sharply after the opening bell, reaching a daily low of 7390.50, and then rose back into the middle range of the day’s decline.

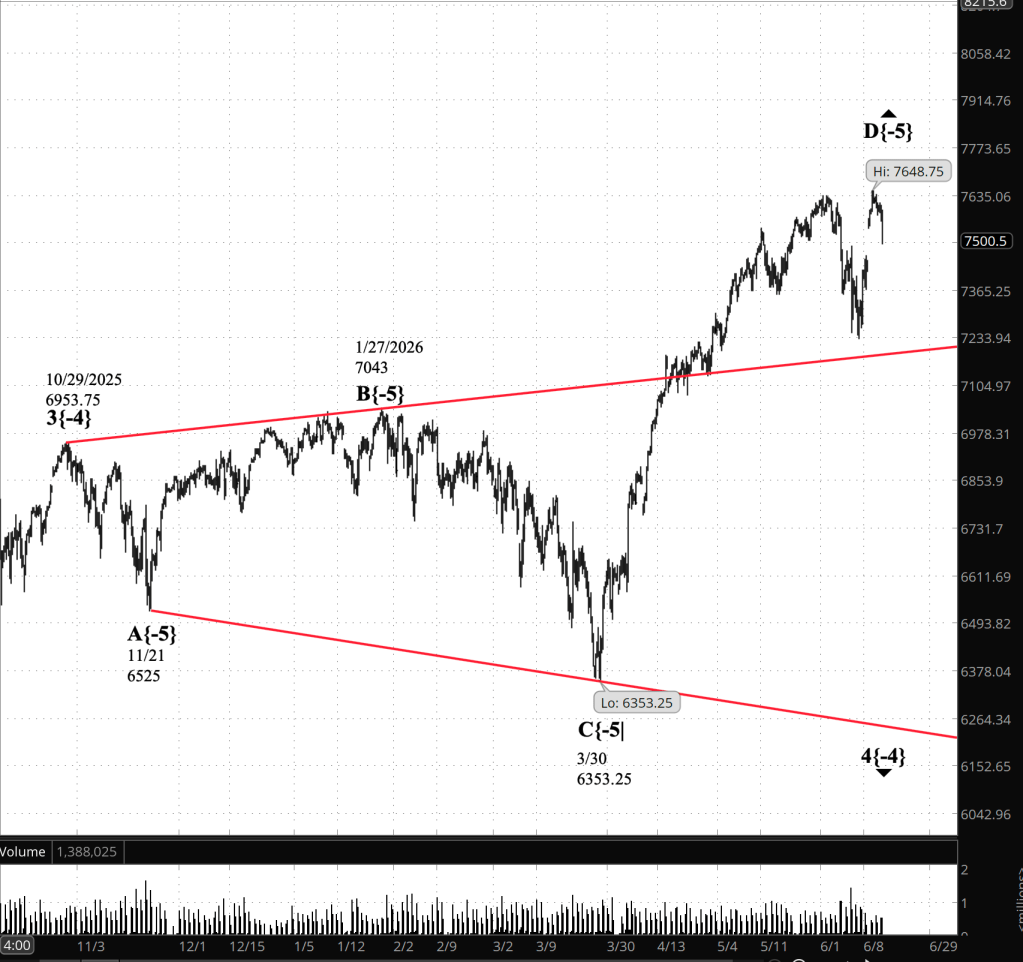

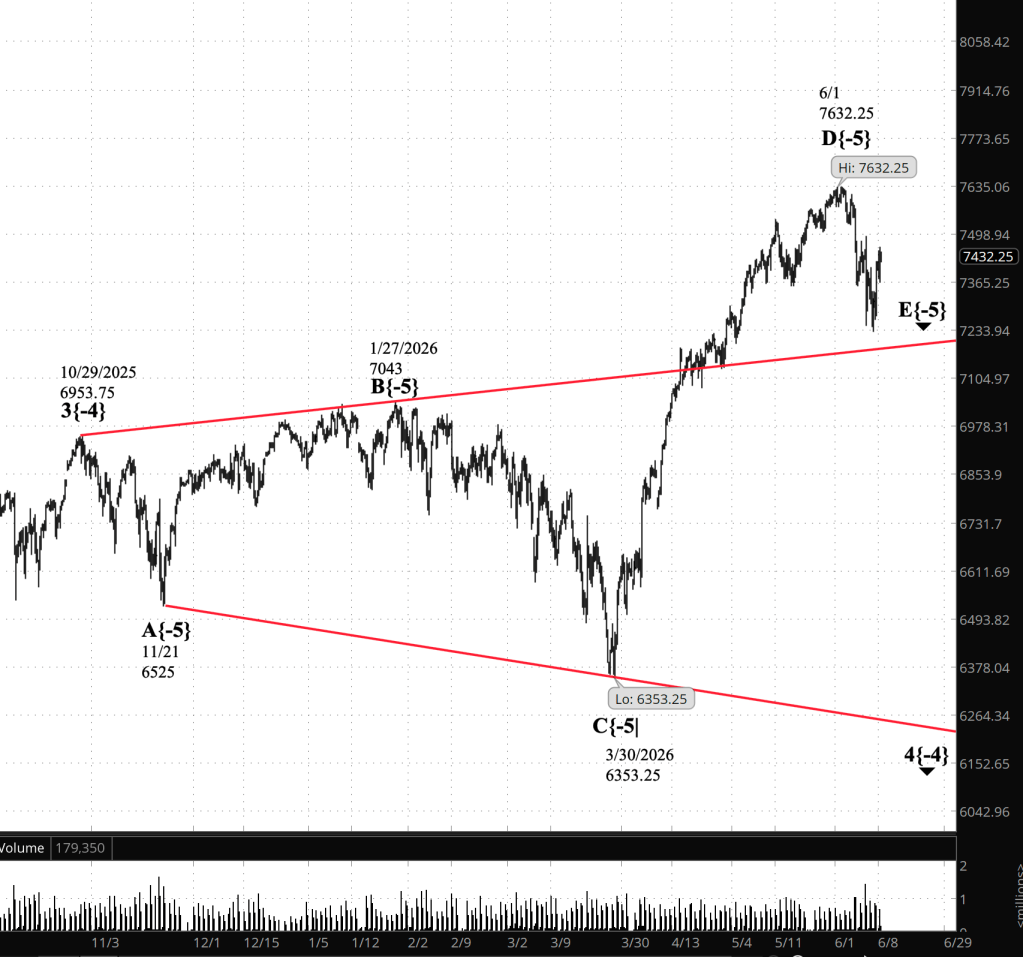

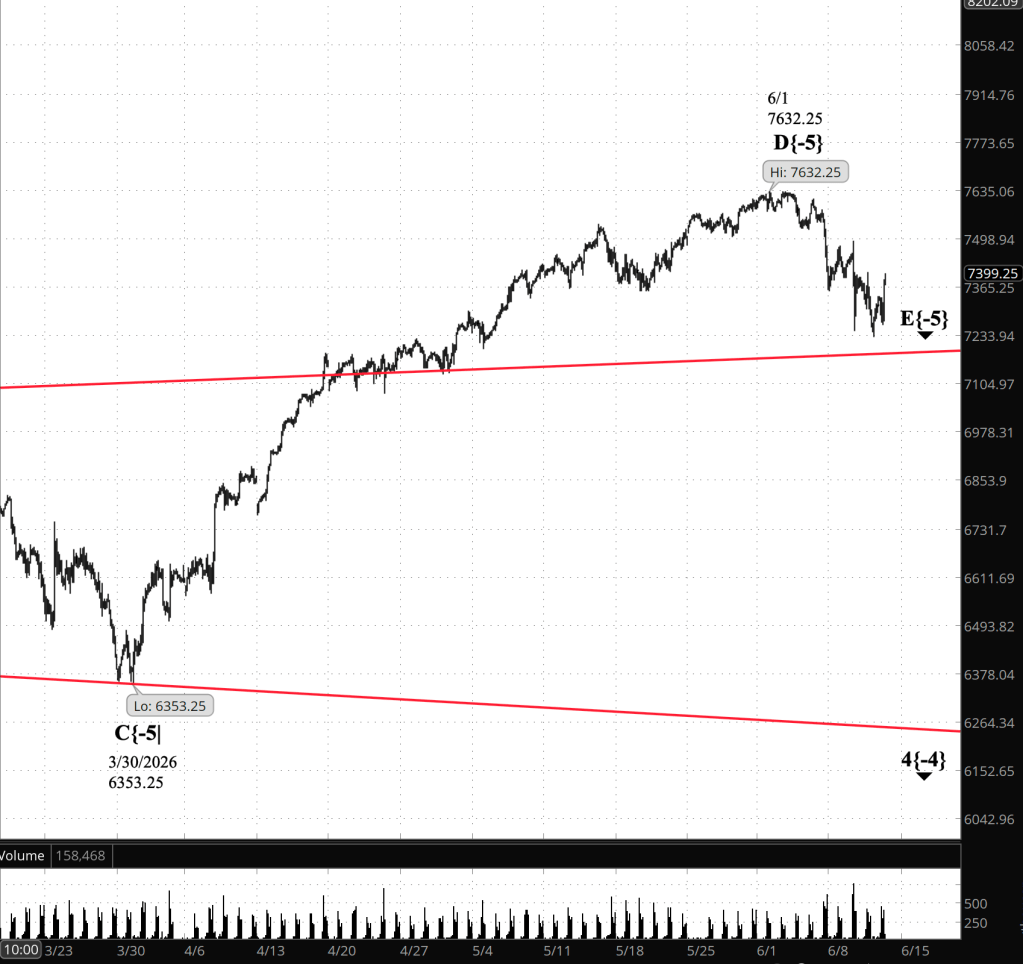

Elliott Wave Theory sees the chart since the June 15 peak, 7648.75, as uncertain, although today’s decline gives more weight to the bearish interpretation. The decline may be a downward correction within rising wave D{-5}, in which case the price will reverse and rise above the June 15 peak. Or the June 15 peak may have marked the end of wave D{-5} and the beginning of falling wave E{-5}, in which case the price will continue to fall toward the lower boundary of the parent wave 4{-4} expanding triangle.

That lower boundary will be near 6200 in late July. In expanding triangles, boundaries formed by connecting earlier turning points often become turning areas for later waves, although the price can turn before reaching the boundary or can break beyond it.

One way to think of the chart is this: the price may still rise enough to continue wave D{-5}, but once wave D{-5} is complete, wave E{-5} will carry the price substantially lower before wave 4{-4} ends.

Decision Points. A rise above 7648.75 would confirm that wave D{-5} is still underway. A decline below the June 11 low, 7232.25, would confirm that wave E{-5} has begun. A fall below today’s low, 7390.50, would not by itself confirm wave E{-5}, but it would increase the likelihood that the June 15 peak was the end of wave D{-5}. Between those levels, the chart remains unresolved.

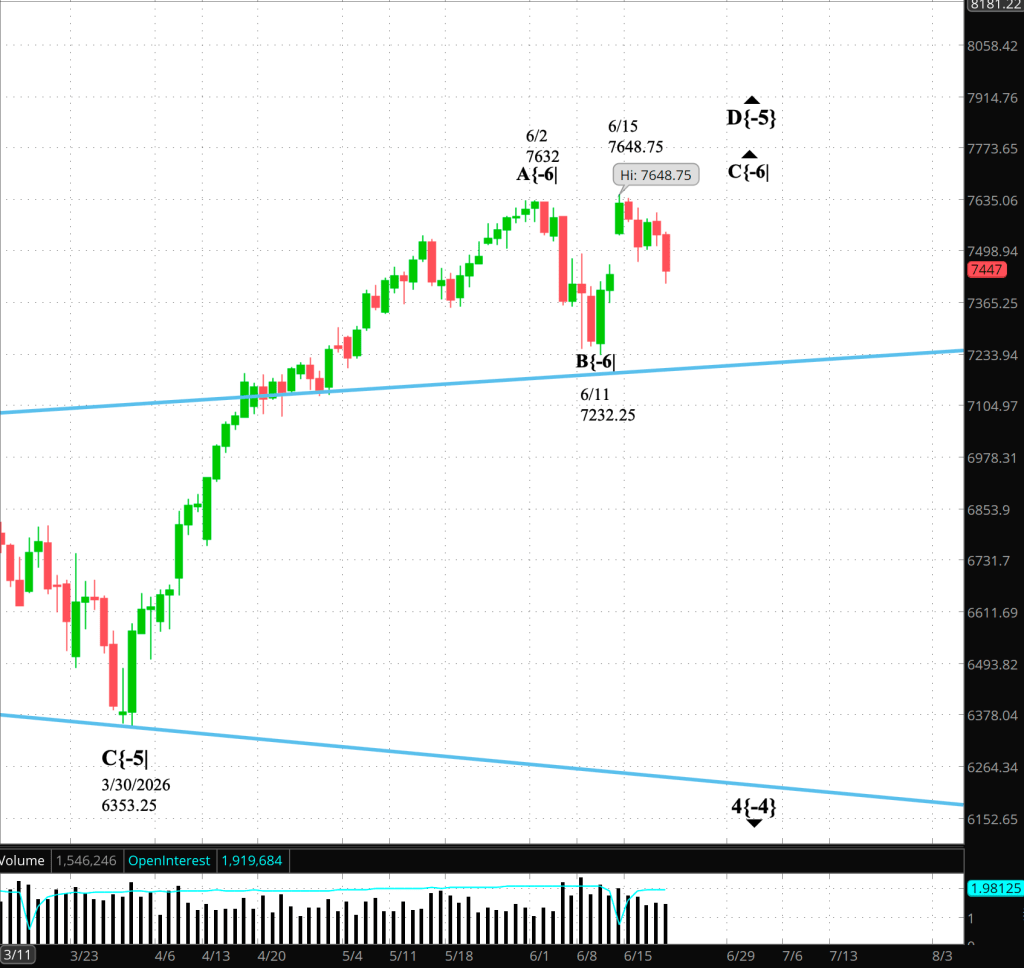

9:35 a.m. New York time

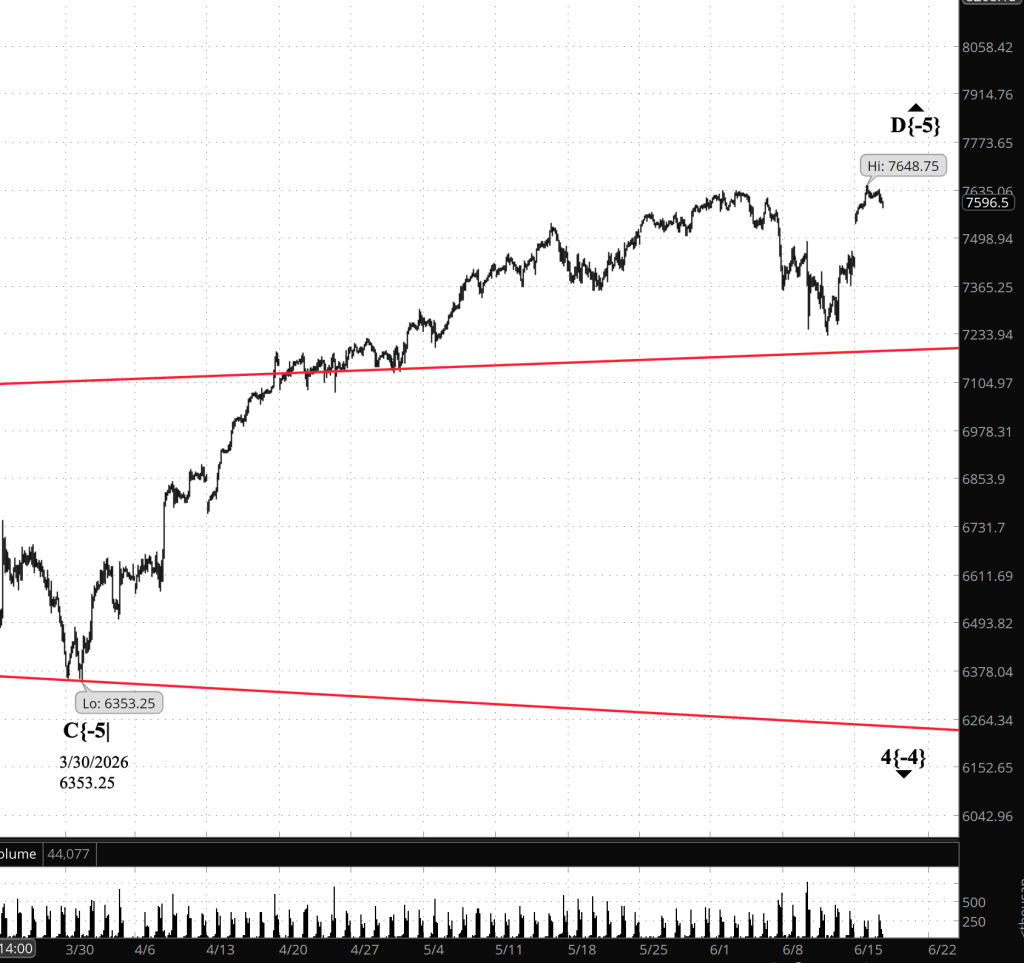

What’s happening now? The S&P 500 E-mini futures fell overnight to a daily low of 7452.25 and then rose, reaching a daily high of 7496. The price remains within the range that has contained trading since the June 11 low and the June 15 high.

What does it mean? Elliott Wave Theory, when applied to the chart, shows little certainty about the present wave structure. Today’s rise, so far, is too small to resolve the ambiguity. The broader fact remains that the price has moved sideways-to-lower since the June 15 high, but without a decline large enough to confirm that wave D{-5} has ended.

The price remains between the June 15 high, 7648.75, and the June 11 low, 7232.25. Until one of those levels is broken, the count remains unresolved: rising wave D{-5} may still be underway, or falling wave E{-5} may have begun from the June 15 high.

Decision Points. A rise above 7648.75 would confirm that wave D{-5} is still underway. A decline below 7232.25 would confirm that wave E{-5}, the final subwave of wave 4{-4}, has begun. Between those levels, the chart calls for patience rather than prediction.

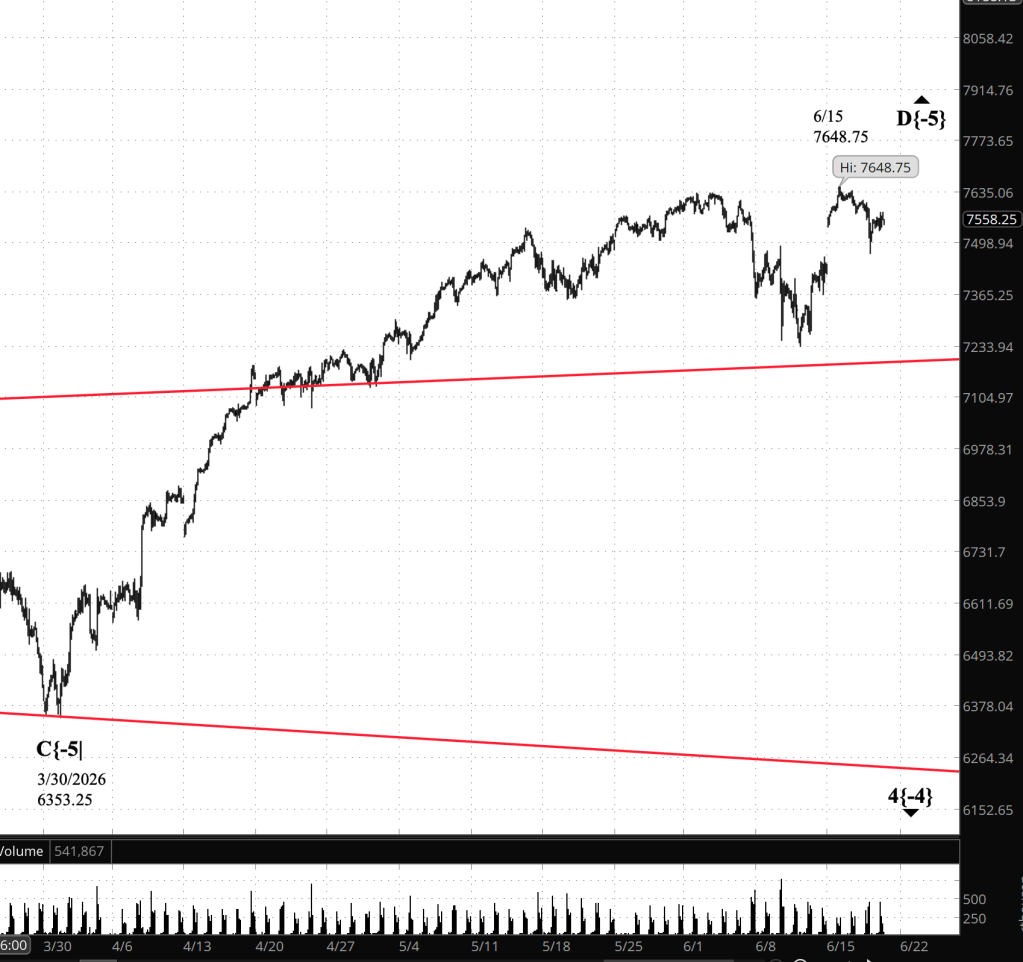

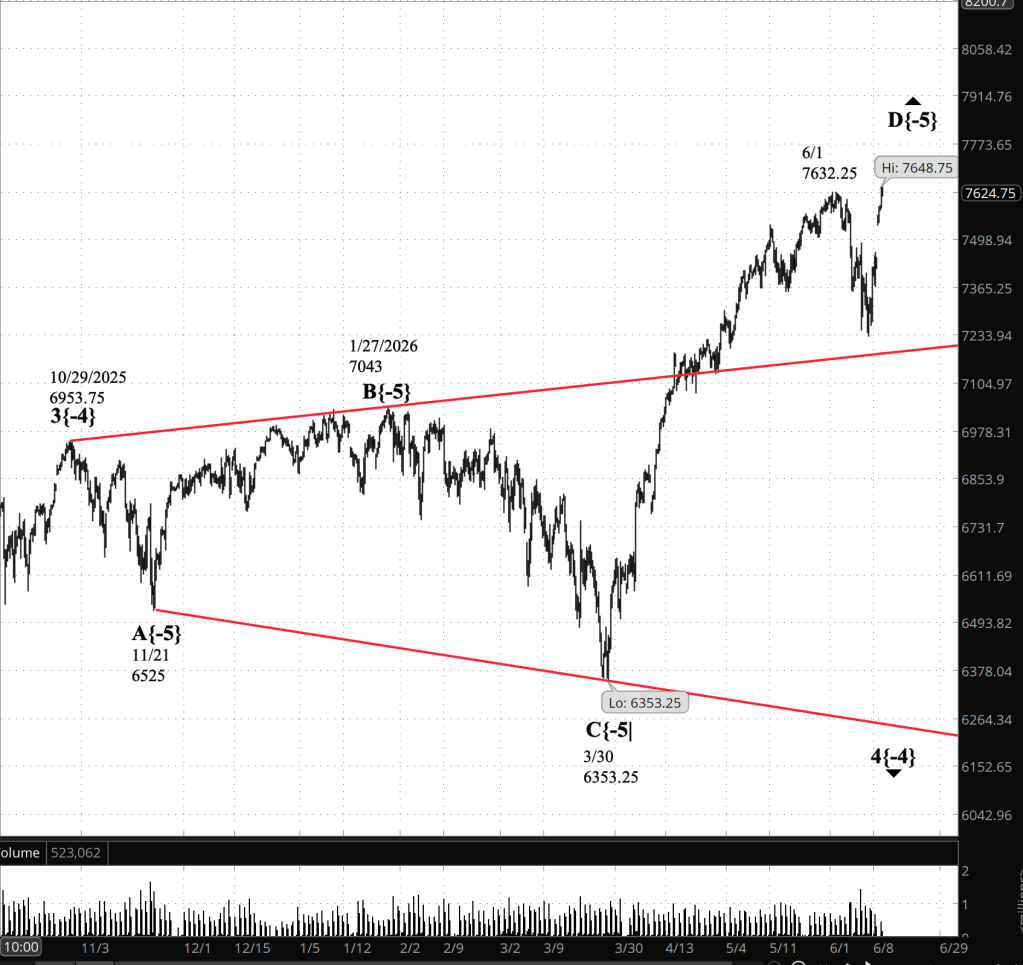

The Chart. Today’s chart focuses on rising wave D{-5}, which began on March 30 and is a subwave of downward correction wave 4{-4}. Wave 4{-4} began on October 29, 2025, and is taking the form of an expanding triangle, a somewhat uncommon form in which each upward swing moves higher than the upward swing before it, and each downward swing moves lower than the downward swing before it.

[S&P 500 E-mini futures 3:30 p.m., 1-day bars with volume]

Waves Now Underway

These are the waves currently in progress under my principal analysis. Each line on the list shows the wave number, with the subscript in curly brackets, the traditional degree name, the starting date, the starting price of the S&P 500 E-mini futures, and the direction of the wave.

- S&P 500 Index:

- 5{+3} Supercycle, 7/8/1932, 4.40 (up)

- 5{+2} Cycle, 12/9/1974, 60.96 (up)

- 5{+1} Primary, 3/6/2009, 666.79 (up)

- 5{0} Intermediate, 2/11/2016, 1810.10 (up)

- 3{-1} Minor, 3/23/2020, 2191.36 (up)

- 1{-2} Minute, 7/31/2025, 6468.50 (down)

- S&P 500 E-mini futures

- 5{-3} Minuette 8/1/2025, 6239.50 (up}

- 4{-4} Subminutte 10/29/2025, 6953.75 (down}

- D{-5} Micro, 3/30/2026, 6353.25 (up}

- C{-6} Submicro, 6/11/2026, 7232.25 (up)

Reading the chart. Price movements — waves – – in Elliott Wave Theory analysis are labeled with numbers within trending waves and letters with corrective waves. The subscripts — numbers in curly brackets — designate the wave’s degree, which, in Elliott Wave analysis, means the relative position of a wave within the larger and smaller structures that make up the chart.R.N. Elliott, who in the 1930s developed the form of analysis that bears his name, viewed the chart as a complex structure of smaller waves nested within larger waves, which in turn are nested within still larger waves. In mathematics it’s called a fractal structure, where at every scale the pattern is similar to the others.

Learning and other resources. Elliott Wave analysis provides context, not prophecy. As the 20th century semanticist Alfred Korzybski put it in his book Science and Sanity(1933), “The map is not the territory… The only usefulness of a map depends on similarity of structure between the empirical world and the map.” And I would add, in the ever-changing markets, we can judge that similarity of structure only after the fact.

See the menu pageAnalytical Methodsfor a rundown on where to go for information on Elliott Wave analysis.

By Tim Bovee, Portland, Oregon, June 25, 2026

Disclaimer

Tim Bovee, Private Trader tracks the analysis and trades of a private trader managing his own accounts. The content reflects my interpretation of market structure, including Elliott Wave Theory and related tools.

Nothing in this blog constitutes a recommendation to buy or sell stocks, options, or any other financial instrument, or to pursue any particular strategy. The purpose of this blog is education and entertainment.

No trader is ever 100 percent successful. Trading in stock and options markets involves risk and uncertainty. Each trader must make decisions for his or her own account and accept full responsibility for the outcomes.

Charts and tools are used to support my personal analysis. Any data displayed is illustrative of that analytical process and is not presented as a source of market data for redistribution.

All content onTim Bovee, Private TraderbyTimothy K. Boveeis licensed under aCreative Commons Attribution-ShareAlike 4.0 International License.

License

Based on work atwww.timbovee.com

You must be logged in to post a comment.