Update 3/18/2020: I exited my short bear call spread position on SPY for 52.1% of maximum potential profit, for $0.68 per contract/share, a profit of $0.74, with the stock trading at $244.92, down $10.60 from the entry price.

SPY hit a peak the day after I entered the position and then declined quickly. The implied volatility rank was 86.5% at exit, down 17.9 percentage points from entry.

Shares declined by 4.2% over six days, or a -18% annual rate. The options position produced a 105.96% return for a +6,620% annual rate.

I have entered a short bear call spread on SPY, using options that trade for the last time 36 days hence, on April 17. The premium is a $1.42 credit and the stock at the time of entry was priced at $255.56

The position is profitable below $288.58.

The implied volatility rank (IVR) stands at 104.4%.

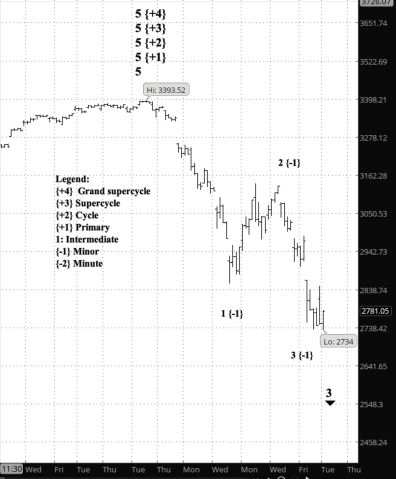

In terms of Elliott wave analysis, the position was opened during Minor wave 3 to the downside.

| Premium: | $1.42 | Expire OTM | |

| SPY-bear call spread | Strike | Odds | Delta |

| Calls | |||

| Long | 296.00 | 90.0% | 11 |

| Break-even | 288.58 | 87.5% | 16 |

| Short | 290.00 | 85.0% | 20 |

The premium is 47.3% of the width of the position’s wing.

The profit zone covers a 12.9% move to the upside and an unlimited move to the downside of the entry price.

The risk/reward ratio is 3.2:1, with maximum risk of $458 and maximum reward of $142 per contract.

By Tim Bovee, Portland, Oregon, March 12, 2020

You must be logged in to post a comment.